Internal capital is the value created by the Bank and the Group for themselves through their activities, relationships and linkages over the period of their existence. It consists of financial capital which is quantifiable and reflected in the financial statements and is available for investments in economic capital and the institutional capital comprising intangibles such as organisational knowledge, systems and processes, corporate culture and values, brand equity, business ethics and integrity and the like, a repository of tacit, explicit and embedded knowledge, which gives the Bank and the Group a competitive advantage in their respective markets. Both these forms of internal capitals help the Bank and the Group to deliver more value to the stakeholders and in return derive value from them, growing these internal capitals further.

Financial Capital

Accounting Framework

The financial statements of DFCC Bank PLC and the Group have been prepared in conformity with the requirements of Sri Lanka Accounting Standards (SLFRSs and LKASs). The SLFRSs and LKASs are aligned with corresponding International Financial Reporting Standards (IFRSs).

Whenever new standards or amendments to existing standards are introduced by The Institute of Chartered Accountants of Sri Lanka (CA Sri Lanka), where appropriate, the Group changes existing accounting policies or introduces new accounting policies. In the event of a change of an existing accounting policy, the relevant accounting standard requires retrospective application of the amended accounting policy. Thus, in the period under review, due to the adoption of the Statement of Alternative Treatment (SoAT) on accounting for Super Gains Tax, the Super Gains Tax which was liable on profits for the year ended 31 March 2014 is deemed to be an expenditure for the year ended 31 March 2014 and as such the Statement of Equity as at 1 April 2015 has been adjusted in accounting for this expense. The impact to the equity due to this adjustment was LKR 777 million (Group LKR 811 million).

In accordance with the provisions of Part VIII of the Companies Act, DFCC Vardhana Bank PLC (DVB) has been amalgamated with DFCC Bank PLC with effect from 1 October 2015 and DFCC Bank survive as the amalgamated entity. Giving effect to the amalgamation, the Registrar General of Companies issued a Certificate of Amalgamation in accordance with the Section 244 (1) (a) of the Companies Act.

DVB was a 99.17% owned subsidiary of DFCC Bank and DFCC Bank consolidated the results of DVB up to the date of amalgamation.

The amalgamation between the two entities is considered as a common control transaction, as DFCC Bank continues to control the operations of DVB after the amalgamation. Thus, the results of amalgamation of the two entities are economically the same before and after the amalgamation as the amalgamated entity will have identical net assets. Therefore, DFCC Bank will continue to record the carrying values (book values) including the remaining goodwill that has resulted from the original acquisitions of DVB in the consolidated statement of financial position.

The legal form of the amalgamation is considered when preparing the separate financial statements of DFCC Bank as the surviving entity. Thus, the carrying values of the assets, liabilities and reserves of DVB is amalgamated with that of DFCC Bank with effect from 1 October 2015. Therefore, no goodwill is recognised in the separate financial statements. The difference between the total investment in subsidiary by DFCC Bank and the stated capital of DVB is adjusted in the Statement of Changes in Equity. Accordingly, on the date of the amalgamation, the investment in DVB of LKR 5,945 million including the balance payment to minority shareholders amounting to LKR 122 million has been set off against the equity of DVB.

Overview of Financial Performance of the Group

Currently, DFCC Group comprises DFCC Bank PLC, its subsidiaries, Lanka Industrial Estates Limited (LINDEL), DFCC Consulting (Pvt) Limited, Synapsys Limited, the joint venture company, Acuity Partners (Pvt) Limited (APL) and the associate company National Asset Management Limited (NAMAL).

Pursuant to the amalgamation, DFCC Bank changed its financial year end from 31 March to 31 December. As such the period results are reported from 1 April 2015 to 31 December 2015.

In the prior years, since the Bank’s financial year ended on 31 March, the results of DVB, APL and Synapsys Limited were consolidated with a three-month gap.

Due to the change of the financial year, the results of these companies with a financial year end of 31 December has now been consolidated after closing the three month gap period of January to March. However, the results of DFCC Consulting (Pvt) Limited and LINDEL whose financial year ends on 31 March have been consolidated for a period of nine months ending on 31 December 2015.

In this review, the period means the nine month period from 1 April to 31 December 2015 and previous year means the year ended 31 March 2015.

As the performance of the period consist of only a nine month period, the results cannot be directly compared with that of the previous year.

Composition of Group Profit Before Tax|

9 months ended 31.12.2015 LKR million |

Year ended 31.03.2015 LKR million |

|||

|

Profit before tax – banking business |

2,450 | 5,176 | ||

| Profit before tax – subsidiaries | ||||

| – LINDEL | 118 | 150 | ||

| – APL (50% share) | 67 | 138 | ||

| – Other subsidiaries | (6) | 14 | ||

| Sub total | 179 | 302 | ||

| – Consolidation adjustment | (88) | (77) | ||

| Total, subsidiaries | 91 | 225 | ||

| Profit before tax, total | 2,541 | 5,401 | ||

| Income tax | (911) | (977) | ||

| Profit after tax – sub total | 1,630 | 4,424 | ||

|

Share of profit – associate company, NAMAL |

12 | 15 | ||

| Profit after tax as reported | 1,642 | 4,439 | ||

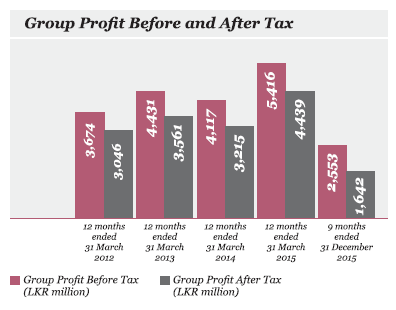

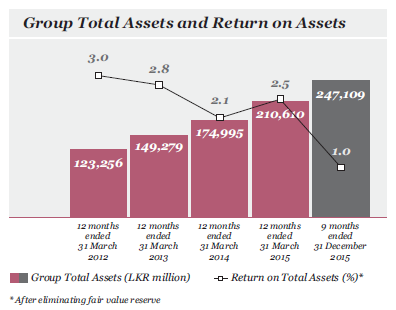

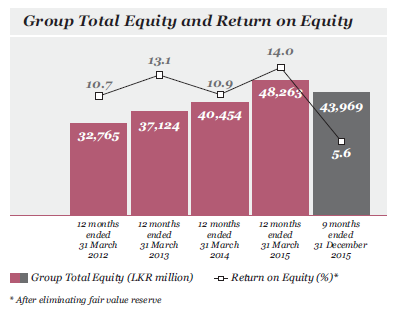

Due to the contracted reporting period, as a result of changing the accounting period to 31 December from 31 March, and the one-off amalgamated related expenses, Group profit before and after tax for the current period reduced to LKR 2,553 million and LKR 1,642 million respectively compared to LKR 5,416 million and LKR 4,439 million in the previous financial year. The Return on Assets (ROA) and Return on Equity (ROE) too decreased to 0.84% and 5.6% respectively in the current period, from 2.5% and 14% respectively compared to the previous year.

However, the total assets of the Group recorded a significant growth of 17% and stood at LKR 247,109 million as at 31 December 2015 compared to LKR 210,610 million on 31 March 2015. Within this growth, loans and receivables to customers grew by 18% over the previous year.

Financial Performance of DFCC Bank and DFCC Vardhana Bank (Banking Business)

By far the largest contribution to profits and assets was from the Banking Business (BB), and therefore, this review will mainly focus on the performance of the Banking Business which is our core business.

For comparison purposes a revised Income Statement and Statement of Financial Position is presented in Notes 61.1 and 61.2 to the financial statements prepared on the basis that the amalgamation took place prior to 1 April 2014.

Profit after tax of BB

The profit after tax of the Banking Business in the period was LKR 1,239 million, compared to LKR 4,501 million in previous year. This is not comparable due to the contracted financial period and the one-off items included in the two periods.

Revenue Mix of BB

Key Components of Income|

9 months ended

31.12.2015 |

Year ended

31.03.2015 |

|||

| LKR million | % | LKR million | % | |

| Net interest income | 5,385 | 76.8 | 6,929 | 63.9 |

| Net fee and commission income | 843 | 12.0 | 1,097 | 10.1 |

| Net gain from trading | 172 | 2.5 | 496 | 4.6 |

| Gain on sale of equity securities | 37 | 0.5 | 1,135 | 10.5 |

| Dividend income | 308 | 4.4 | 991 | 9.1 |

| Fx income | (40) | -0.6 | (113) | -1.0 |

| Others | 306 | 4.4 | 309 | 2.8 |

| Total operating income | 7,011 | 100.0 | 10,845 | 100.0 |

Total operating income was LKR 7,011 million in the nine months ended 31 December 2015, compared to LKR 10,845 million in the previous year.

The net interest income (NII) was LKR 5,385 million which translates to a 3.6% growth on an annualised basis, compared to LKR 6,929 million reported in the previous year. The Bank witnessed interest margin dropping to 3.1% during the nine months period ended 31 December 2015 from 3.6% in March 2015 due to lower interest rates prevailed in the environment. NII, which is the main source of income from the fund-based operations represent over 77% of the total operating income of the Banking Business.

In spite of the very healthy credit portfolio growth of over 15% achieved by the Banking Business during the current 9 month period, the NII growth was depressed due to the higher drop in lending rates in comparison to the drop in the deposit rates.

Net fee and commission income of BB in the period under review was LKR 843 million compared to LKR 1,097 million in the previous year. On an annualised basis, it translates to a marginal increase of 2.4% compared to the previous year. Fee and commission income is derived largely from the banking services provided to customers engaged in import and export business, fees from guarantees issued on behalf of customers engaged in trade and construction activities and commission income from other banking services.

Net gain from trading in the period under review was LKR 172 million compared to LKR 496 million reported in the previous year. Due to upward trend in the market interest rates for fixed income securities, less income was realised from fixed income capital gains during the period compared to the previous year.

Gain on sale of equity securities was LKR 37 million in the period under review compared to LKR 1,135 million in the previous year. The drop was mainly due to the adverse market conditions prevailed during that period. Previous year gains were significantly high due to one-off capital gain of LKR 829 million realised on the divestment of the entire holding of 9.92% ordinary voting shares of Nations Trust Bank PLC.

Dividend income received by the Bank makes a significant contribution to other income. This is derived largely from the investment in Commercial Bank of Ceylon PLC supplemented by dividend from other equity securities which classified as available-for-sale. However, due to the financial year end being advanced to 31 December 2015, dividend declared during the first quarter of 2016 is not included in the results of the period.

The forward exchange contracts are accounted as a derivative and its fair value changes are reported as net gain/(loss) from financial instruments at fair value through profit or loss in the income statement. Other forward exchange gains/losses are reported under other operating income.

Foreign exchange income too did not contribute positively towards the profit of the period under review due to the depreciation of the Sri Lankan Rupee against the US Dollar. However, the overall foreign exchange contribution reported a positive variance during the period compared to the previous year due to the reduction of the negative open exposure and the reduced cost from the foreign exchange swaps carried out in order to benefit from higher yielding Rupee assets.

Composition of Operating Expenses

|

9 months ended 31.12.2015 |

Year ended 31.03.2015 |

|||

| % | % | |||

| Personnel cost | 52.6 | 50.8 | ||

| Depreciation and amortisation | 6.9 | 8.4 | ||

| Others | 40.4 | 40.8 |

Operating expenses of BB was LKR 3,883 million compared to LKR 4,218 million in the previous year. Approximately half of the operating expenses are on account of personnel compensation (current and deferred compensation relating to retirement). In common with the banking industry, personnel cost is a significant proportion of the operating expenses. Due to stringent cost management, operating expenses excluding personnel cost increase was not significant. This increase was largely due to costs associated with branch expansion, merger related expenses and general price increases. Due to the relatively young branch network the contribution from the new members in the network is lower compared to the more mature branches. These costs incurred on expansion of branch network will be eventually recovered by additional revenue generation by these new branches in the years to come.

Impairment allowance charge to the income statement is high in the period compared to what was reported in the previous year. This is mainly due to a reversal in impairment allowance in the previous year arising from a change to the impairment assessment process.

Income tax liability is based on the accounting profit computed under SLFRSs adjusted for disallowable expenses and exempt income as per the provisions of the Inland Revenue Act No. 10 of 2006 (as amended).

In common with Banks, DFCC Bank is liable for Value Added Tax (VAT) and Nation Building Tax (NBT) on financial services (effective rate 11.5%) and income tax (nominal rate 28%). The value addition from the supply of financial services is computed as the accounting profit plus salaries minus economic depreciation on assets replacing accounting depreciation. Value Added Tax and NBT on financial services are non-deductible expenses for computing the taxable profit for income tax purposes.

The Bank has received approval under Section 28(4) of the Inland Revenue Act, to adopt the calendar year (1 January to 31 December) as the basis of accounting year commencing from the Year of Assessment 2015 - 2016. Accordingly, the Bank has computed statutory income for Year of Assessment 2015 - 2016 including results for 12 months despite the reported results relate only to a period of nine months. As a result an estimated income tax liability of LKR 180 million is included under the current period tax on account of the change in the financial year.

The total of VAT and NBT on financial services and income tax expense as a percentage of profit before these taxes was 50% in the financial period compared with 31% in the previous financial year. The additional tax expense due to the change in financial year to December has resulted in a 8% increase in tax expense of the Bank for the period.

Credit Quality

Analysis of Impaired Loans| As at |

9 months ended 31.12.2015 |

Year ended 31.03.2015 |

| LKR million | LKR million | |

| Impaired loans to customers | 8,554 | 8,658 |

| Impairment allowance | 6,166 | 6,010 |

| Ratios: | ||

|

Impairment allowance/impaired loans (%) |

72.1 | 69.4 |

| Impaired loans/total loans (%) | 5.1 | 6.1 |

The ratio of impaired loans to total loans on 31 December 2015 was 5.1% compared to 6.1% on 31 March 2015, indicating an improvement in credit quality. The cumulative allowance for impairment for loans and advances of BB was maintained at a healthy level of 72.1% as at 31 December 2015. The impairment allowance coverage for impaired loans is adequate when fair value of the underlying collateral is taken into account.

Due to the different computation methodologies, the ratios of NPL and provision coverage under regulatory regime are not comparable with SLFRSs regime.

The SLFRSs based impairment assessment, both individual and collective, is to a large extent based on historical evidence modified by an experience adjustment by management, to take into account current economic conditions. Interest income is recognised on an accrual basis and therefore, impairment allowance is for both principal and interest.

Aggressive recovery efforts throughout the year have consistently driven down the ratio of impaired loans to total loans as well as the regulatory NPL ratio of the Bank. Regulatory NPL ratio reported for the Bank as at end of December 2015 is 3.7% compared to 4.3% in the previous year.

Composition of Total Assets

| As at |

9 months ended 31.12.2015 |

Year ended 31.03.2015 |

||

| % | % | |||

| Earning assets | ||||

| Loans to and receivable from customers | 65.1 | 64.1 | ||

| Loans to and receivable from banks | 1.9 | 1.8 | ||

| Other interest-earning financial assets | 7.3 | 7.7 | ||

| Available-for-sale investments | 19.9 | 21.2 | ||

| Non-earning assets | ||||

| Property, plant and equipment | 0.4 | 0.4 | ||

| Intangible assets | 0.1 | 0.1 | ||

| Others | 5.3 | 4.7 | ||

| Total assets | 100.0 | 100.0 |

Of the total assets 92% were denominated in Sri Lanka Rupees and the balance comprised mainly in US Dollar denominated assets. Total assets of BB recorded a healthy growth of 14% and amounted to LKR 246,151 million as at 31 December 2015 compared to LKR 215,919 million as at end of the previous year.

Gross loans and advances reported a significant growth of 15% recording LKR 171,085 million as at end of 31 December 2015 compared to LKR 148,433 million recorded in the previous year.

Listed shares are classified as available-for-sale and carried at fair value. Fair value changes that represent unrealised gains/loss are recognised in other comprehensive income. During the period ended 31 December 2015, due to adverse market conditions the available-for-sale securities recorded a fair value loss of LKR 3,158 million. In the comparable year, the fair value gain was LKR 5,595 million.

Composition of Interest-Bearing Liabilities

| As at |

9 months ended 31.12.2015 |

Year ended 31.03.2015 |

||

| LKR million | % | LKR million | % | |

| Borrowing sourced from: | ||||

| Multilateral lending agencies | 22,581 | 11.4 | 18,949 | 11.5 |

| Bilateral lenders | 4,162 | 2.1 | 5,413 | 3.3 |

| International capital market | 14,528 | 7.3 | 13,746 | 8.4 |

| Domestic capital market | 12,026 | 6.1 | 6,810 | 4.1 |

| Debenture issue private placement | 506 | 0.3 | 526 | 0.3 |

| Borrowing from banks | 13,345 | 6.7 | 8,081 | 4.9 |

| Customer deposits | 110,891 | 55.9 | 91,782 | 55.8 |

| Repos | 20,232 | 10.2 | 19,248 | 11.7 |

| Total | 198,271 | 100.0 | 164,555 | 100.0 |

Liabilities are mainly in Sri Lanka Rupees but it also has foreign currency liabilities, mainly US Dollars. Remarkable growth of 21% was achieved in customer deposits during the nine months ended 31 December 2015 compared to the previous year.

In June 2015, DVB successfully raised funds with a tenor of five years by way of unsecured redeemable rated debenture, which was listed in the Colombo Stock Exchange. A significant feature of the issue was that there were two types of debt offered in the same issue (i.e., senior and subordinated). Accordingly, the Bank raised LKR 3 billion by way of senior debt and LKR 2 billion as subordinated debt. The issue was oversubscribed on the first day itself.

The USD 100 million five year notes issued to non-resident investors in October 2013 continues to be supported by the Government with a foreign exchange cover up to USD 75 million from the Central Bank of Sri Lanka (CBSL), to neutralise any change in exchange rates.

The accounting treatment is based on the recognition and measurement criteria of forward exchange USD purchase contract, a derivative asset and recognition and measurement of income grant by Government via CBSL.

Profit Contribution from Members of the Group

This comprises the profit contribution from LINDEL and DFCC Consulting (Pvt) Limited for the nine months ended 31 December 2015 and Synapsys Limited, APL and NAMAL for 12 months ended 31 December 2015. Amongst the subsidiaries, LINDEL continues to be profitable with a return on investment of 22% during the financial period compared with 24% during the previous financial year. The profit contribution from the other members was LKR 72 million.

Financial Assistance Received from Government

The Government has acted as a conduit for direct funds raised from multilateral and bilateral agencies for lending to eligible sectors. The amount outstanding on 31 December 2015 was LKR 23.2 million.

The exchange loss cover provided by the Central Bank of Sri Lanka is a de-facto grant to the extent of USD 75 million international note issue.

The Government does not own direct equity, but entities over which the Government exercises control have continued to own shares of DFCC Bank. As of 31 December 2015, the aggregate shareholding was approximately 35%.

Critical Accounting Policies and Estimation of Uncertainties

The results of DFCC Bank and the Group are sensitive to the accounting policies, assumptions and estimates that underlie the preparation of financial statements.

Directors have the responsibility to select suitable accounting policies and to make judgments and estimates that are reasonable and prudent. These accounting policies, judgments etc. are explained in the notes to the financial statements.

Current Year Changes and Impending Changes to Financial Reporting

These are disclosed in notes to the financial statements.

Management of Equity

Dividend Performance

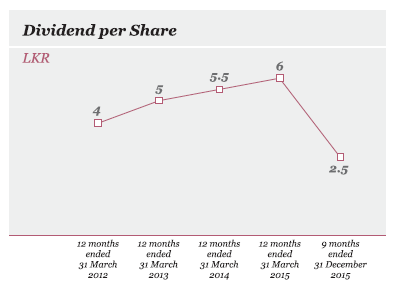

The payout ratio based on the dividend approved by the Directors is 62% in the period under review compared to 49% in the previous year.

Dividend per share for the nine months ended 31 December 2015 is LKR 2.50 per share compared to LKR 6.00 per share in the previous year. The decrease in the dividend is mainly due to the financial results for the period being for a contracted period of nine months.

Return on Equity

Return on equity of the Group for the period was 4%. The equity of the Group is significantly augmented due to the recognition of unrealised gains on listed ordinary shares and Government Securities classified under available-for-sale as required under SLFRSs and the resultant increase in equity on 31 December 2015 is LKR 11,858 million. The return on equity will improve to 5.6% if this unrealised gain is not taken into account.

Return on equity is expected to improve with expansion of earning assets financed with borrowing. DFCC Bank will balance higher risk associated with gearing with the need to hold capital cushion commensurate with risk and maintain a prudent dividend distribution policy.

Regulatory Minimum Capital Requirement

DFCC Bank’s capital is well over the minimum requirement (refer Note 65.6).

The regulatory capital computation excludes fair value changes of financial assets classified as available-for-sale. Bank continued to remain as one of the best capitalised Banks in the industry with Group Tier 1 capital adequacy ratio at 15.39% and total capital adequacy ratio at 15.32%.

Financial Value Added

The total value added by DFCC Bank during the nine months ended 31 December 2015 amounted to LKR 3,303 million (year ended 31 March 2015: LKR 5,440 million). Details of value added and distributed are given under Supplementary Information on Value Added Statement and Sources and Distribution of Income sections.

INSTITUTIONAL CAPITAL

Institutional capital entails a broad spectrum of non-financial intangible components of capital that are unique to DFCC Bank. It includes organisational knowledge, systems, processes and ICT, corporate culture and values, brand equity and business ethics and integrity, all of which are important elements in creating sustainable value for our stakeholders.

Organisational Knowledge

Being in operation for 60 years, we have been able to perfect our competencies in every area, especially when it comes to project financing. We have developed a team of diverse multi-skilled professionals, and our knowledge and expertise is one of the major value drivers of our business. The result has been, a strong reputation of being a comprehensive service provider and the first choice for any new venture or expansion project whether it is on a large or small scale.

We have used our expertise to provide sustainable development financing, especially in the rural areas, helping to transform rural economies and support and bolster livelihoods, generate employment and encourage capital formation in every district in Sri Lanka. The World Bank recognised DFCC Bank as being one of a small number of development finance institutions that was not only viable but also successful in transforming itself into a multi-product, strong financial institution in a changing international and local environment.

Today, we have amalgamated with our commercial banking subsidiary, DFCC Vardhana Bank, and have transformed into a fully-fledged commercial bank. We draw synergies from our complementary areas of business through our subsidiaries, joint venture and associate company. These services include consultancy, industrial estate management, IT services, investment banking, stockbroking and venture capital and management of unit trusts.

We will continue to develop capabilities and build stronger and more profitable relationships by providing customised solutions, leveraging synergies across our main businesses and capitalising on our core strengths whilst nurturing our most valued assets; our employees.

Systems, Processes and ICT

Our internal systems and processes are developed with a strong focus on innovation, and Information Technology plays a vital role in executing day-to-day operations of the Bank. As a result of the amalgamation, many of our systems and processes were revamped in order to increase efficiency. We are continuously improving our management information system in order to make sound strategic decisions.

The initiatives implemented during the period under review are as follows:

- Replacement of an old Lotus Note based Loan Origination system with a web based Facility Origination Workflow solution, to manage the credit approval workflow originating from the branch network and flowing up to the level of the Board of Directors.

- Broadbasing the utility payment solution with the addition of more utility providers and corporates, facilitating the island wide cash collections from consumers/agents to be transmitted online to their respective back-end systems. Moreover, the fund transfer capability of utility payments/agency collections through the Online Banking solution has enabled the customers to manage transactions from their desktops. Requests for Letters of Credit (LC) facilities have been enabled through the Online Banking solution for corporate clients facilitating a faster service.

- Successful consolidation of the two core banking solutions by migrating data from DFCC Bank to DFCC Vardhana Bank to facilitate the amalgamation of the two institutions into one commercial bank. Similarly the Oracle Financials ERP solution went through a consolidation process for financial reporting on the amalgamated entity.

- Launching a supplier settlement solution developed by Synapsys for a leading tea factory covering the automation of the entire life cycle from weighing of tea leaf collections from smallholders, and effecting tea leaf supplier payments through the Bank to facilitating cash withdrawals from the ATM network.

- Development of the Mobile Wallet solution developed by Synapsys, which will facilitate the management of wallet accounts by bank/non-bank customers using a mobile application. This mobile application will facilitate transfer/cash top-ups, merchant payments, fund transfers between wallet accounts, utility payments and a host of other features.

Corporate Culture and Values

With the launch of the new entity, a new vision, mission and a set of values were introduced. A cross-functional team was appointed to give in their recommendations to the Board in this regard, and a company-wide survey was also carried out. This demonstrates the Bank’s team culture, where every individual is directly involved and accountable in realising the Bank’s overall vision.

Our corporate culture and values are derived from our new vision which is ‘to be the leading financial solutions provider sustainably developing individuals and businesses’. Ours is a culture that values professionalism, teamwork, openness, diversity, respect for individual values and recognition; each individual is respected, rewarded and recognised for his/her competence, capabilities and knowledge. We assess not just what people have achieved, but also how they have achieved it, in doing so encouraging sustainable performance.

Our core values are: being innovative, customer centric, professional, ethical, accountable, team oriented and socially responsible.

Brand Equity

The DFCC Bank brand is a heritage brand that has been established as a pioneer and risk taker, nurturing entrepreneurs, businesses and sectors in their early and risky start up stages. The Bank’s clientele consisted of mainly businesses looking to fulfil their project financing needs.

Following the amalgamation, DFCC Bank updated its positioning as a comprehensive financial solutions provider that enables all its stakeholders to ‘Keep Growing’ by providing responsible and innovative financial solutions. Leveraging its development banking and commercial banking expertise, the Bank serves a variety of clients ranging from individuals, professionals and entrepreneurs to SMEs and corporates across the country, operating through 137 branches and service points, and is committed to driving financial inclusion. We are careful to maintain our brand equity at favourable levels and constantly monitor the performance of our brand. The DFCC Bank brand will keep evolving to stay relevant for the future, focusing on sustainable progress and prosperity for all.

Business Ethics and Integrity

DFCC Bank is uncompromising in its adoption of the highest ethics and integrity. Being ethical is one of our key values, and drives our every strategy and action. We have a comprehensive governance mechanism in place and the Corporate Governance Report explains these measures in detail.

Anti-Corruption

Given the negative consequences associated with corruption and also in the interest of our reputation and maintaining transparency, the Bank has a written Code of Conduct that, inter alia, includes provisions relating to anti-corruption. It is not just for legal compliance, but we view it as an ethical issue and a business imperative. In order to ensure collective action by all in the Bank, these provisions have been explained to all staff and are reinforced through updates and monitored throughout all business operations. We are a responsible corporate citizen. We are proud of our unblemished track record in this sphere and it aids our resolve to make our operations sustainable into the future.

Compliance

Being a financial service intermediary, the need to ensure full compliance with the applicable laws, rules and regulations cannot be overemphasised. All of us in the Bank and the Group understand our responsibility in this regard. Our policies and procedures in fact go beyond the legal/regulatory requirements and embrace broader standards of integrity and ethical conduct. Compliance is embedded into our organisational culture. We understand the gravity of non-compliance and the risks associated therewith. Measures taken to manage such risks are detailed under Operational Risk of this Report.

In this sphere too, we maintain a clean scorecard. We have not been informed of any fines or actions by the regulators in relation to any incidents of non-compliance with laws and regulations pertaining to corruption, anti-competitive behaviour, anti-trust, monopoly practices, provision and use of products and services and similar infringements during the period under review.